Table of contents

- Understanding SM REITs

- Eligibility Criteria of Investment Manager

- Migration of Existing Schemes to the SM REIT

- Asset Size and Minimum Investment

- Schemes Within an SM REIT

- Disclosure in Offer Letter

- Equity, Leverage and Asset Mix

- Fundraising and Subscription process

- "Skin-in-the-game" requirements for fund manager

- Distribution of Cashflows

- Valuation of Assets

- Conclusion

There has been a huge buzz in alternate investments space about the launch of SM REITs. It seems like finally SEBI noticed the increasing AUM of Fractional Ownership platforms, and decided to do something about it.

SM REITs are like a smaller version of traditional REITs, which are present in the market for quite some time. But they have many different rules and regulations, that sets them apart from traditional REITs. In this article, we will try to breakdown the newly issued set of regulations for SM REITs and summarize the important points, so you don't have to read the entire document.

If you want to understand the current landscape of fractional ownerships, you can check out our previous blog here, where we discuss everything there is to know about fractional real estate platforms in India.

Understanding SM REITs

Essentially, SEBI is hoping to regulate the existing, and quite thriving market of fractional real estate. Currently, platforms pool investors money to buy a property through an SPV (LLP / Pvt. Ltd). The rental income which is generated throughout the life of the property is distributed to the investors, and at the maturity, the property is sold, and the realized cash is paid to investors in the form of principal + capital gain.

Now, this entire process was unregulated, as SEBI did not have any regulation for small and medium scaled platforms. Only the larger players such as Mindspace, Embassy etc, with an asset size of 500cr+ were allowed to form a REIT via regulated route. SM REIT license aims to solve this problem by regulating smaller platforms currently operating in this space.

To understand these regulations further, let's take a look at some of the important details of the circular, to understand more about this upcoming scheme.

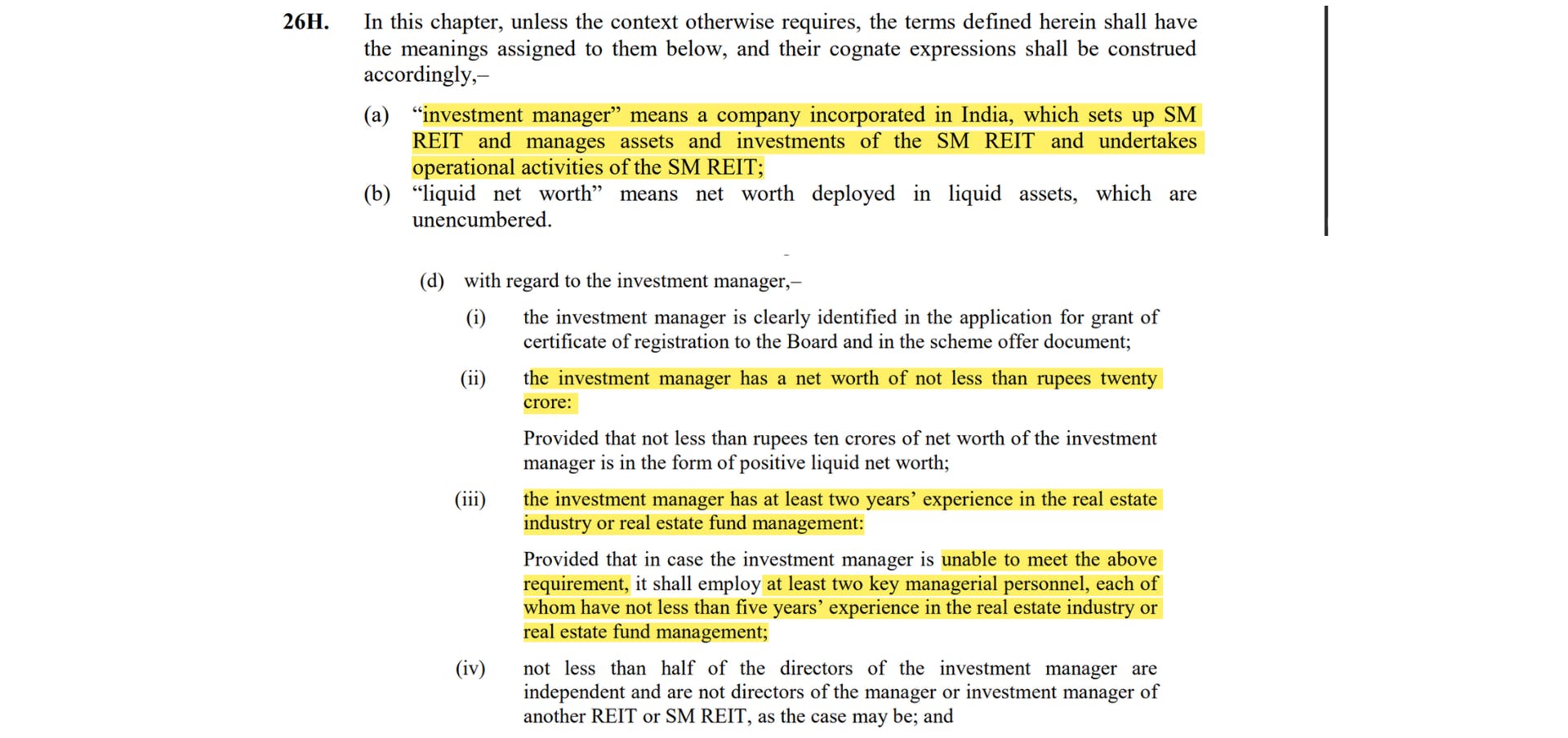

Eligibility Criteria of Investment Manager

To launch a SM REIT, the experience of the investment management company should be at least 2 years, or they should employ someone who has an experience of at least 5 years in Real-Estate space. Their platform should have a net worth of ₹20 Cr which is a steep number.

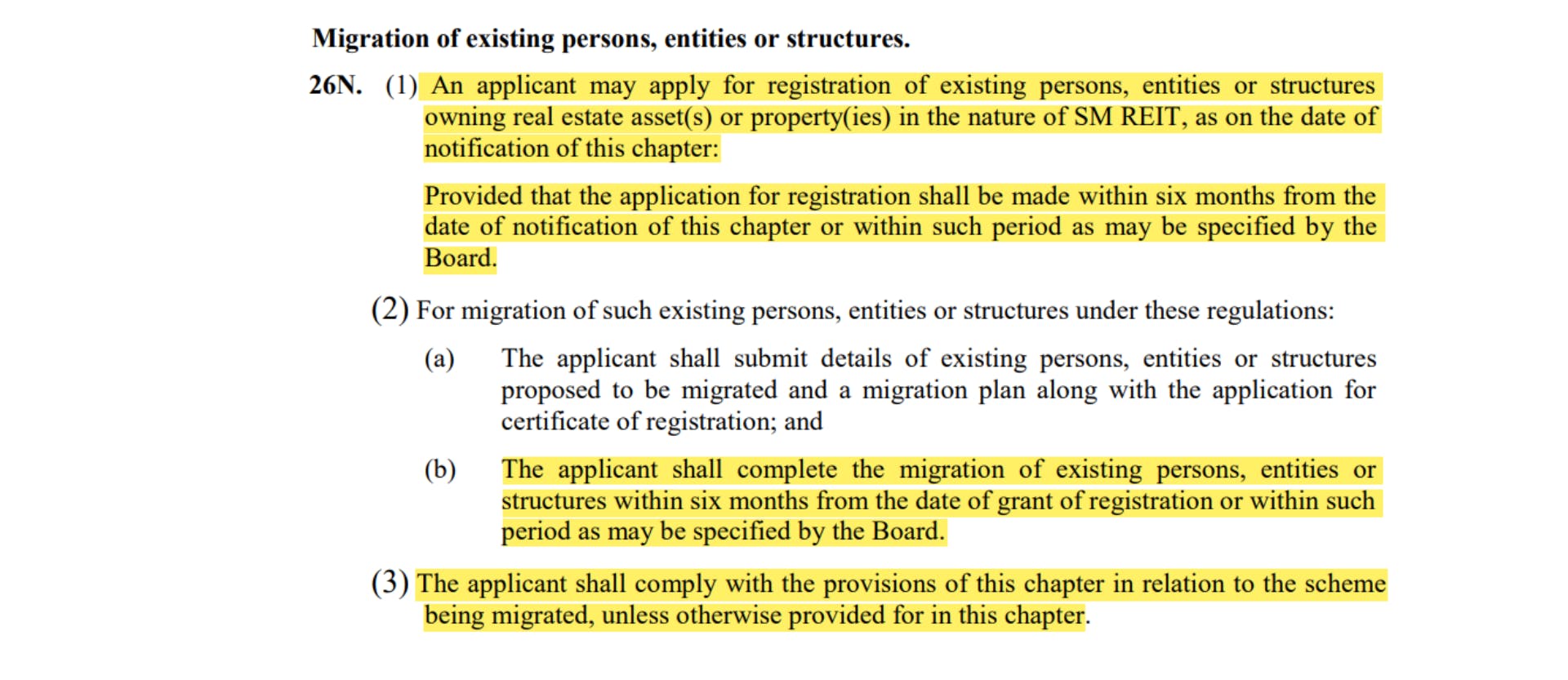

Migration of Existing Schemes to the SM REIT

From what we can understand from below migration clause, the investment managers should transfer properties from their previous fractional real estate SPV transactions to the newly established SM REITs, within the first 6 months of the registration with the regulator.

The real estate properties and the asset sizes will obviously have to comply with the SM REITs norms which are mentioned further down below.

But a lot of industry participants have queried the regulator if it would be mandatory to seek the registration if their overall asset size is less than ₹50 Cr, it's a bit of a grey area which we are still awaiting to hear back from the regulator.

Asset Size and Minimum Investment

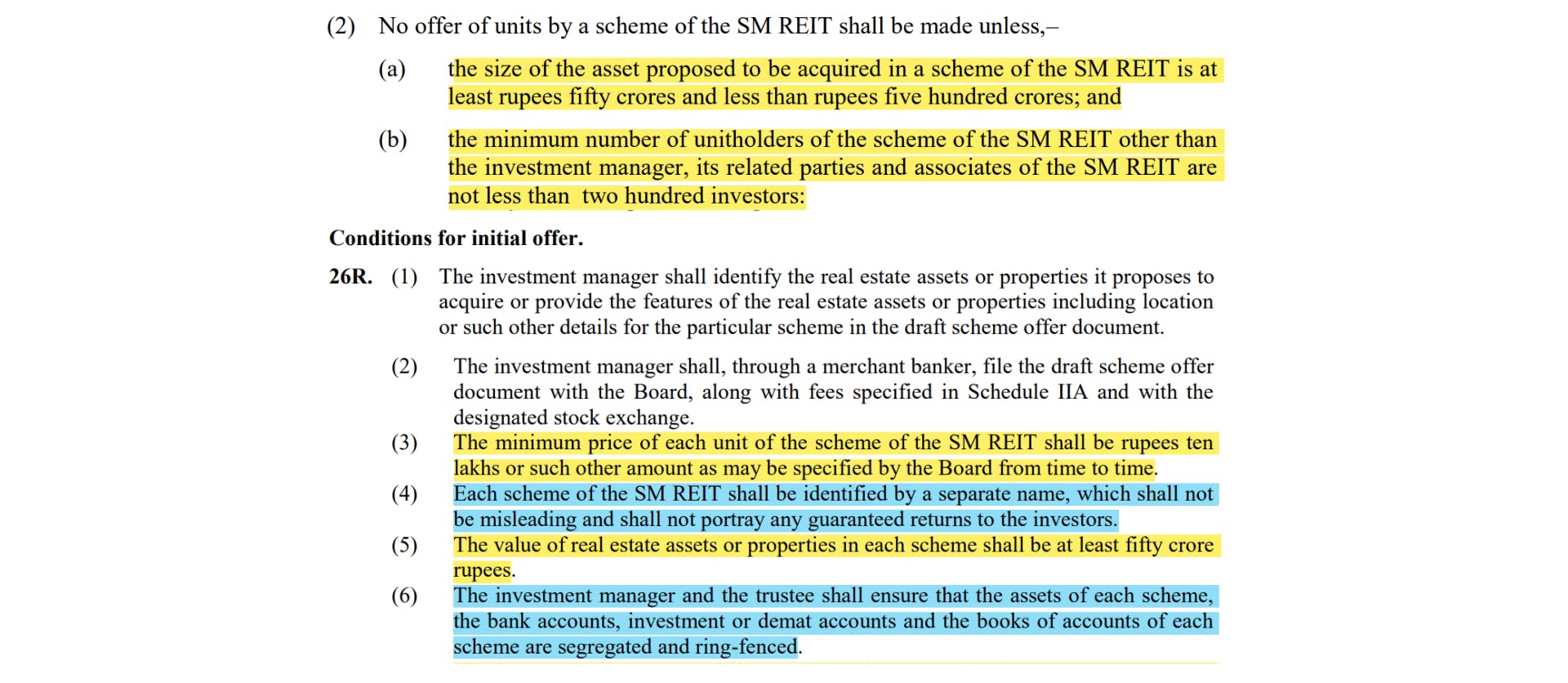

The asset size of a scheme in the SM REIT has to be between ₹50cr - ₹500cr. And the minimum ticket size per unit, which is still quite high, is set at ₹10 Lakh. Also, according to the regulations, 95% of the total assets of the scheme has to be invested in revenue-generating constructed properties.

While the ticket size has reduced from the current ₹25 Lakh to ₹10 Lakh, this is still a large number and we are unsure how liquid the SM REITs will be once listed on the exchange. The current listed REITs have no such minimum investment requirement.

The portion marked in yellow talks about the asset and ticket size, while the one in blue actually talks about the schemes in an SM REIT which we will discuss in the next half.

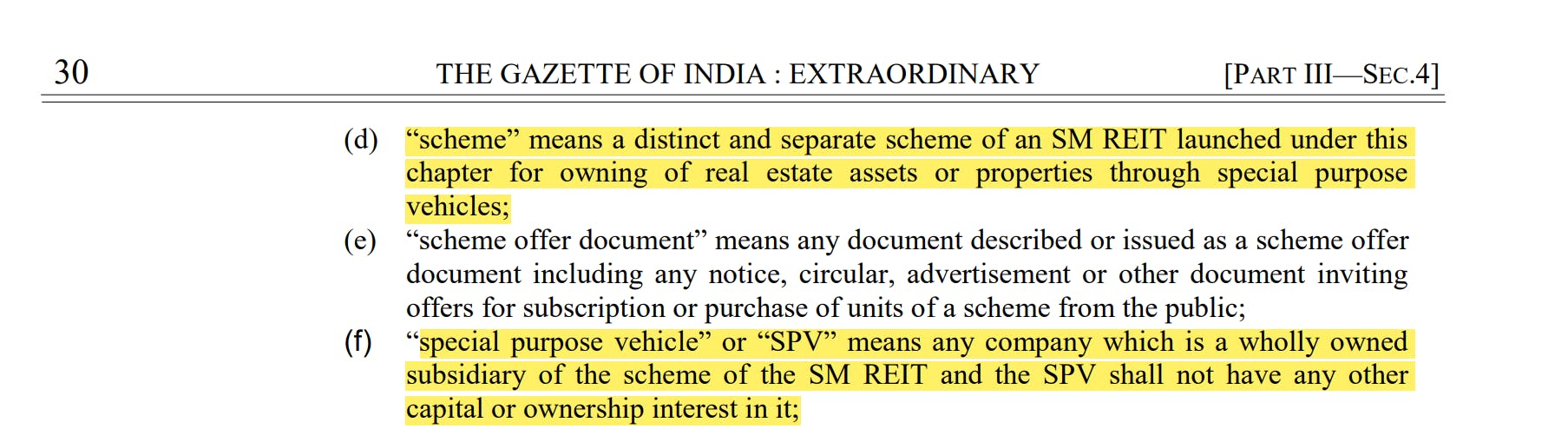

Schemes Within an SM REIT

Our interpretation of the regulation is that one SM REIT can house various SPVs and various different schemes under it. Just like one mutual fund can have various schemes such as small cap, mid cap etc. SM REITs can also have schemes such as warehouse schemes, commercial property schemes, residential real estate schemes etc.

According to this circular, each scheme should have minimum ₹50cr in assets, and obviously, the accounts, returns and balance sheets of each scheme needs to be ring-fenced to separate them from each other. (Above image in blue)

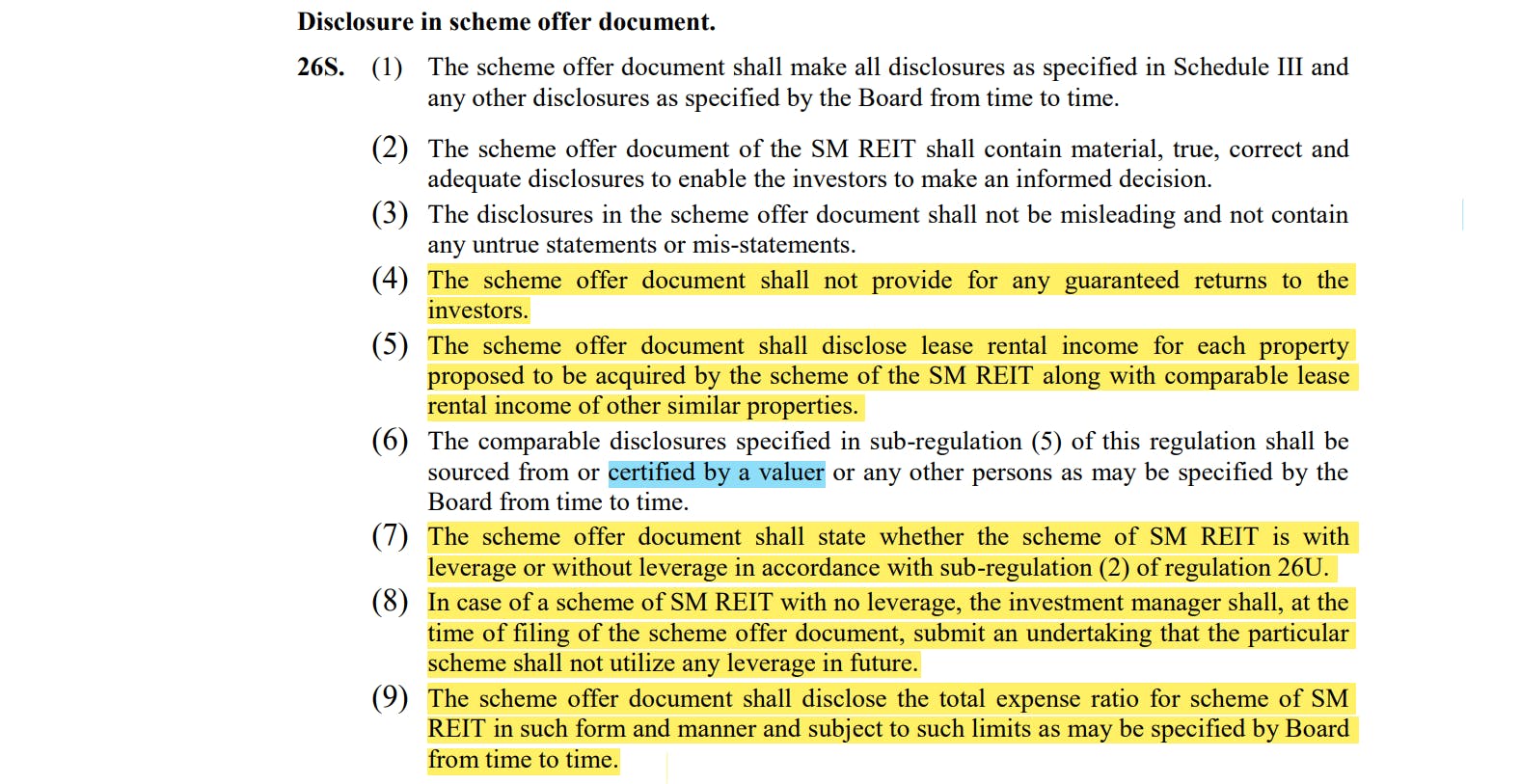

Disclosure in Offer Letter

The offer letter, just like any IPO or NFO must contain key details of the deal. For this SEBI always prepares a guideline as to what needs to be compulsorily mentioned in the document. According to this section, the key points that needs to be highlighted are

Lease rentals (If any negotiated) or comparable lease rentals from neighboring properties.

No guaranteed returns should be mentioned in the offer document.

The scheme needs to disclose whether it plans to take leverage or not

Expense ratio has to be mentioned, and needs to be communicated time-to-time if changed.

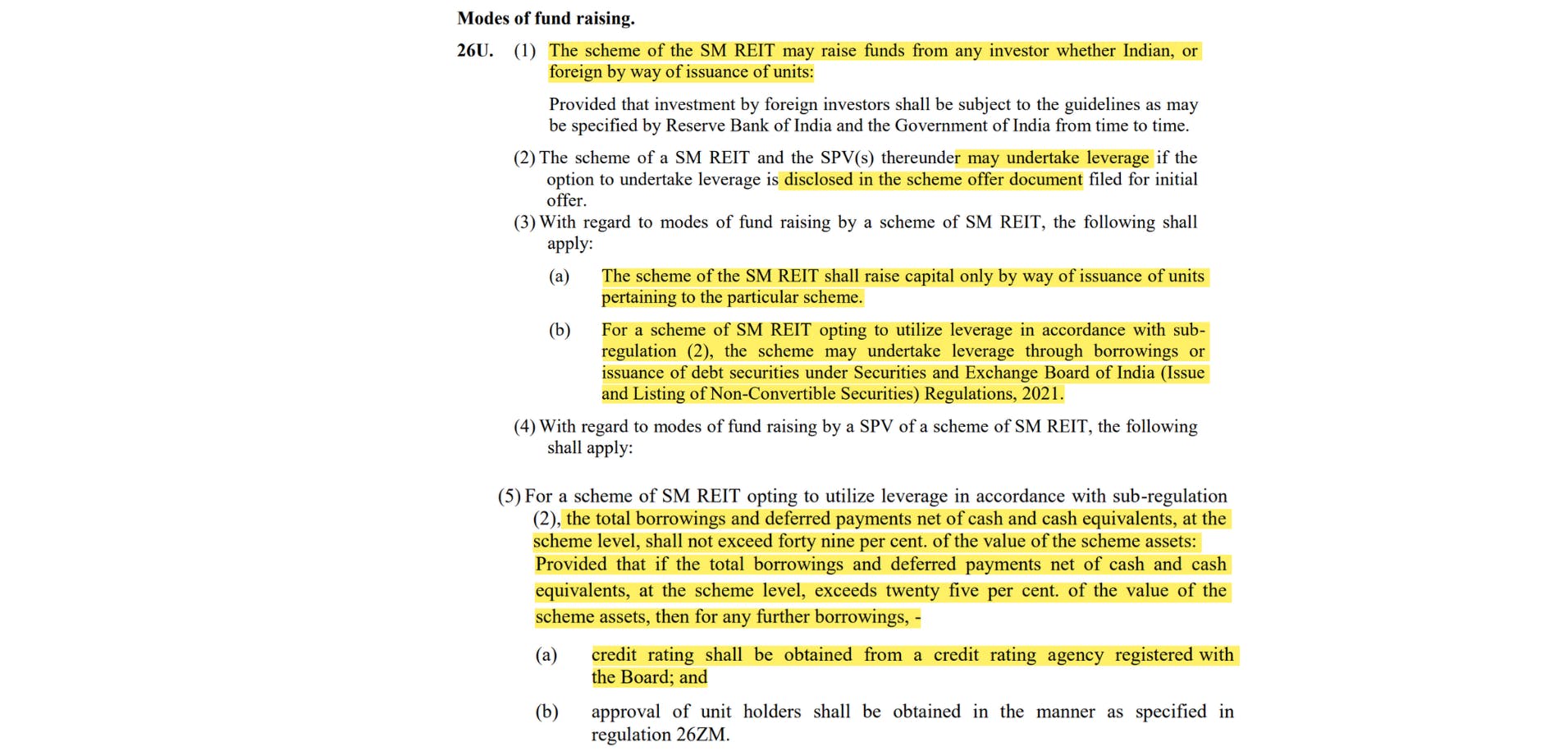

Equity, Leverage and Asset Mix

The individual schemes in the SM REITs can maintain debt upto 49% of the total assets. If the net-debt (Net of cash and equivalent) of the scheme exceeds 25% of the asset value, then a credit rating agency needs to be appointed to give a credit rating to the scheme.

While this is good for the investor, this might increase compliance cost of bringing the SM REIT to the market possibly resulting in lower yields.

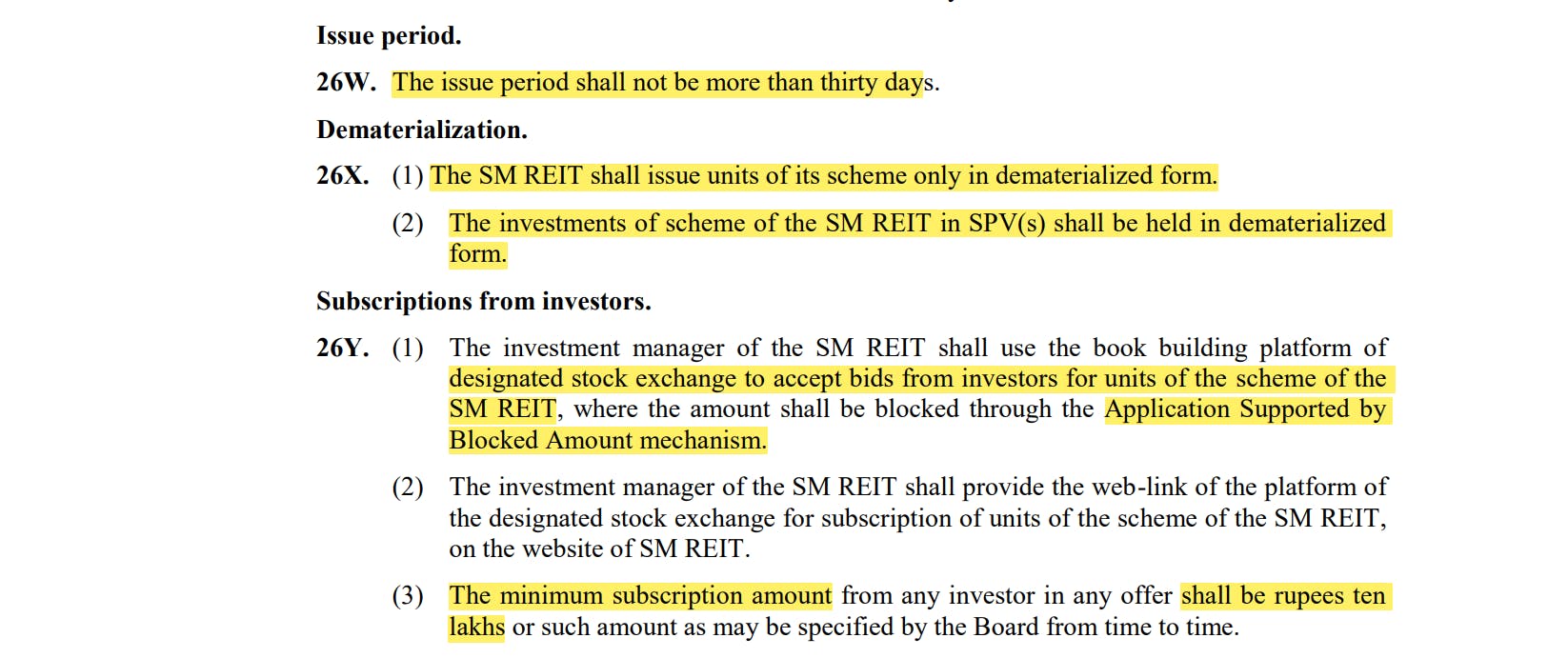

Fundraising and Subscription process

Just like the IPO and equity shares, the units of the SM REIT will be issued in Demat form. The subscription will be done through book-building process with the help of ASBA registration. These units can be traded on the designated stock exchanges just like equity shares, although the liquidity will be questionable.

The funds are raised via SM REIT, which will then invest the proceed into the SPV or the scheme. The SM REIT will also hold the shares/units of the SPV in Demat form.

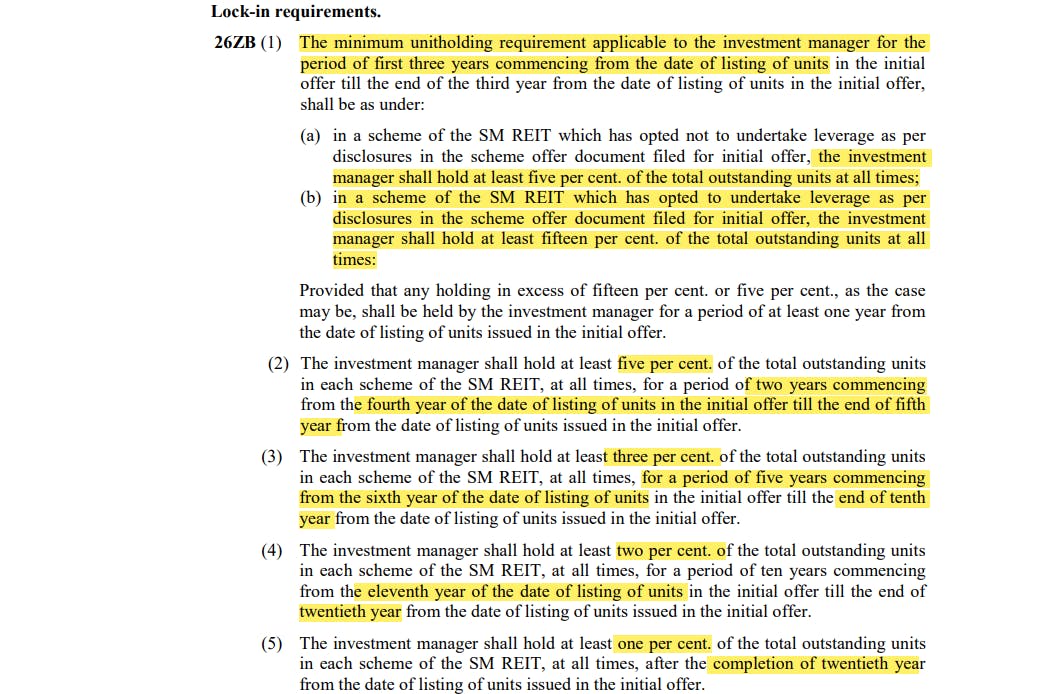

"Skin-in-the-game" requirements for fund manager

This is an interesting part of SM REITs regulation, where SEBI has mandated investment managers to hold a certain percentage of the fund for few years, to ensure that managers are operating in the interest of investors. In this case, the managers have to hold atleast 5% units of the SM REIT for the first 5 year. This number increases to 15% if the SM REIT has opted for leverage.

These holding percentages come down after 5th year, and keep on decreasing to end at 1% till 20th year.

While this is great, but practically we think this maybe challenging for the platform as they already need to have a ₹20 Cr net worth requirement and on top of that let's say their asset size is ₹100Cr with leverage, they need to put up another ₹15 Cr minimum. The platforms might not have that kind of money and may have to reach out to NBFCs or financiers who will want to get a cut as well. This might again result in offering less yields to the end customer but with better security.

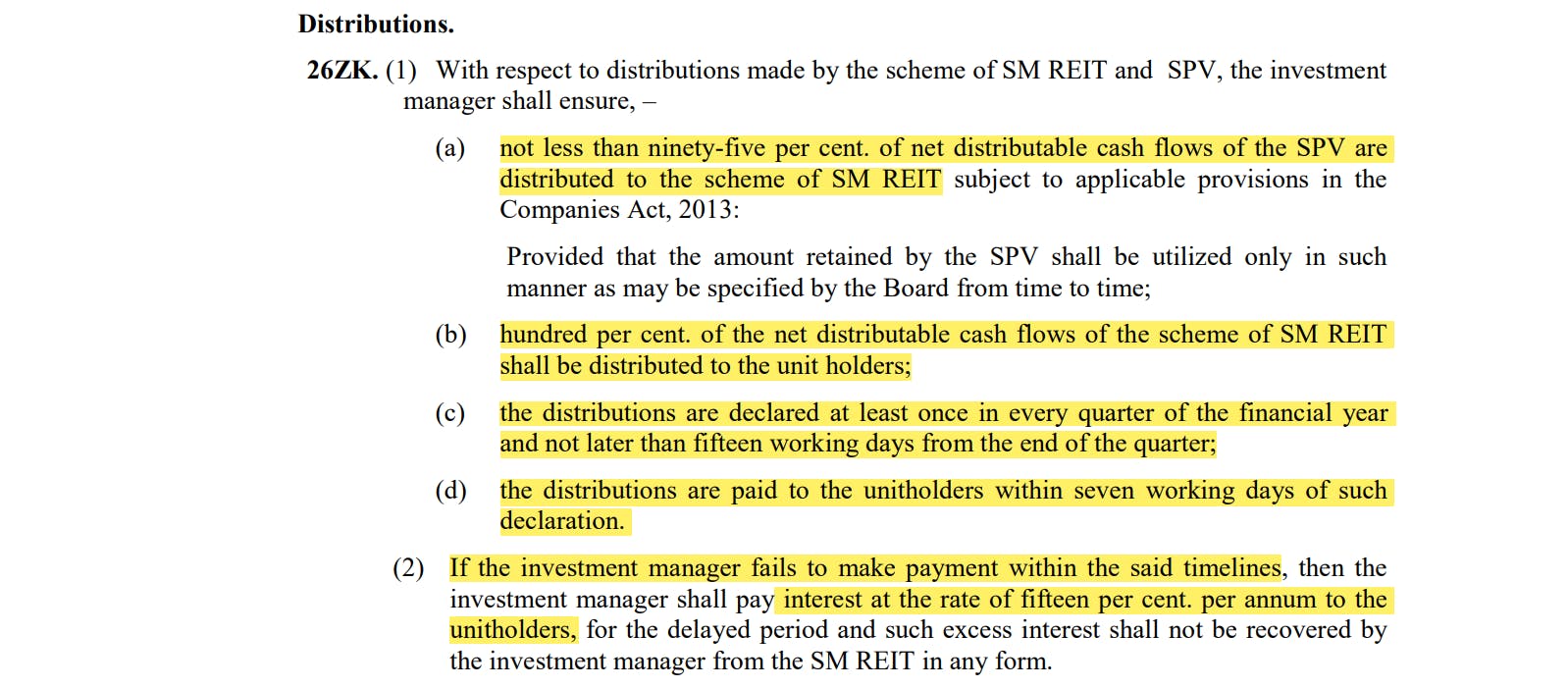

Distribution of Cashflows

To protect investor's interest in the cashflows, SEBI has mandated each scheme to transfer 95% of the cashflows of the SPV to the SM REIT. The rest 5% can be kept as cash or liquid securities.

The SM REIT on the other hand, has to transfer 100% of the cashflows it receives from the Schemes (SPVs) to the investor.

The declaration of income statement needs to be updated every quarter, and within 7 days of declaration of the numbers, the cashflow has to be transferred to the investors.

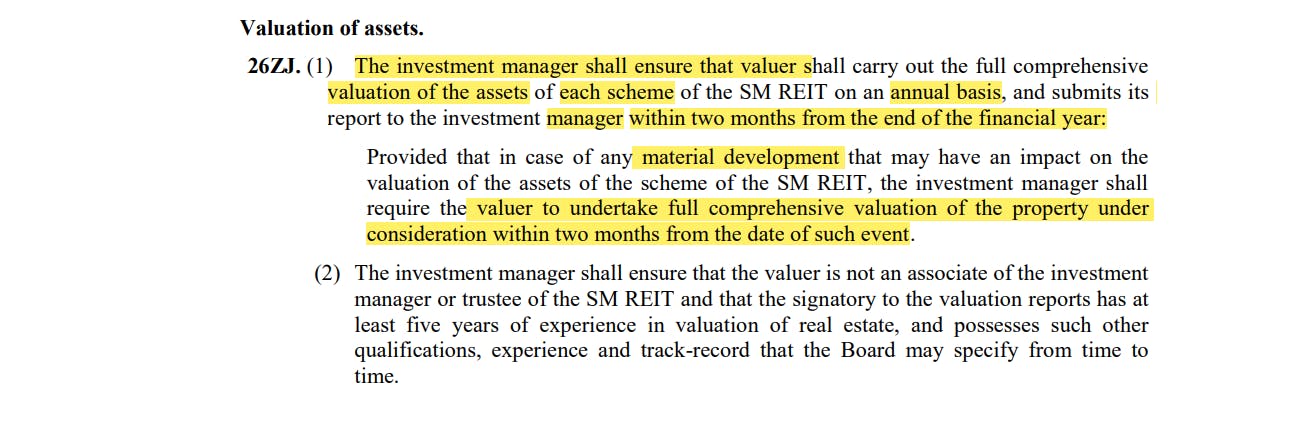

Valuation of Assets

The valuation of the assets of individual scheme has to be done by a certified valuer on annual basis. This will help determine the NAV of each unit, thus offering transparency to the investors along with better price judgment in the markets. But again, I don't understand how the pricing will work on the exchange once it gets listed. Will it be a fixed price which everyone can buy/sell on until a new valuation is derived or something else, it's unclear.

Conclusion

The above list of clauses we covered, should give you decent enough idea, as to how the SM REITs will function in the coming years. But this regulation dictates how SEBI wants FRE platforms to look like, but who knows how the application of these regulation will pan out in the real markets.

One more thing that we have realized after talking to couple of FRE platform owners that to bring a security to exchange, they generally have to seek help from an investment banker or merchant banker who will charge around 6-7% of the overall asset value as fees, the platforms unfortunately don't earn that much money in such deals and the economics might not work out for them at all. Given this regulation is still new, it's a wait and watch to see how it unfolds.

The idea behind this regulation, as we have highlighted before, is to regulate the small and medium scale fractional real estate platforms. These regulations will bring a huge asset size under SEBI's purview, which will help increase transparency and protect investor's interest. But these regulations will also deepen the market of fractional real estates, as more investors will now find the comfort to invest in this space, who were earlier hesitant due to the unregulated nature of these platforms.

That's it for this one. If you find this article helpful, please do like it and share it on Social Media so our blogs get promoted more on Google Searches. If you would like to join our exclusive spam-free WhatsApp community, you can apply here.

Please note that this is an opinion blog and not official research advice. I am not a registered RIA in India. This blog aims to promote informed decision-making and does not discourage you from investing in any deals.

We plan to come up with more blogs discussing different types of instruments available in the world of startup investing, write on due diligence for some platforms, and also existing and upcoming alt investment deals in the Indian market. If you want to stay updated on the latest blogs, please subscribe to our newsletter so you get notified automatically.

Lastly, if you like our work, please feel free to sponsor us via Hashnode Sponsors.