We all have heard about Mutual Funds and most of us must have invested in at least one of the schemes. Thanks to the hyperactive marketing campaigns by AMFI and a catchy tagline of - Mutual Fund Sahi Hai, this investment product found a great traction amongst investors, specifically the retail segment. But when it comes to Indian HNIs, who want to invest crores of their surplus funds, Mutual fund can be a boring category. It's because they already have a lot of wealth tied in equities and debt market and now, they want to try something new. These individuals usually look for something which is not correlated to markets and give them higher risk adjusted returns. So where do they go to invest? A mutual fund for the ultra-rich called Alternate Investment Fund (AIFs).

Some Context And Numbers

Traditionally alternative investments include products such as Venture Capital, Private Equity, Debt Funds, Hedge Funds, Real-Estate Funds etc.

In 2012, SEBI first launched the regulations for AIF funds. The idea was to regulate all the private pooling of funds. Private money from family offices, UHNIs, corporates etc. have been the key driver of AIFs in India. One of the key reasons to regulate this space was to drive capital towards the economically and socially desirable sections of the economy. Startup investing, Corporate and Municipal debt, and Infrastructure funding were some of the highly desirable fields where government was keen to increase the flow of capital, and AIFs provided just that.

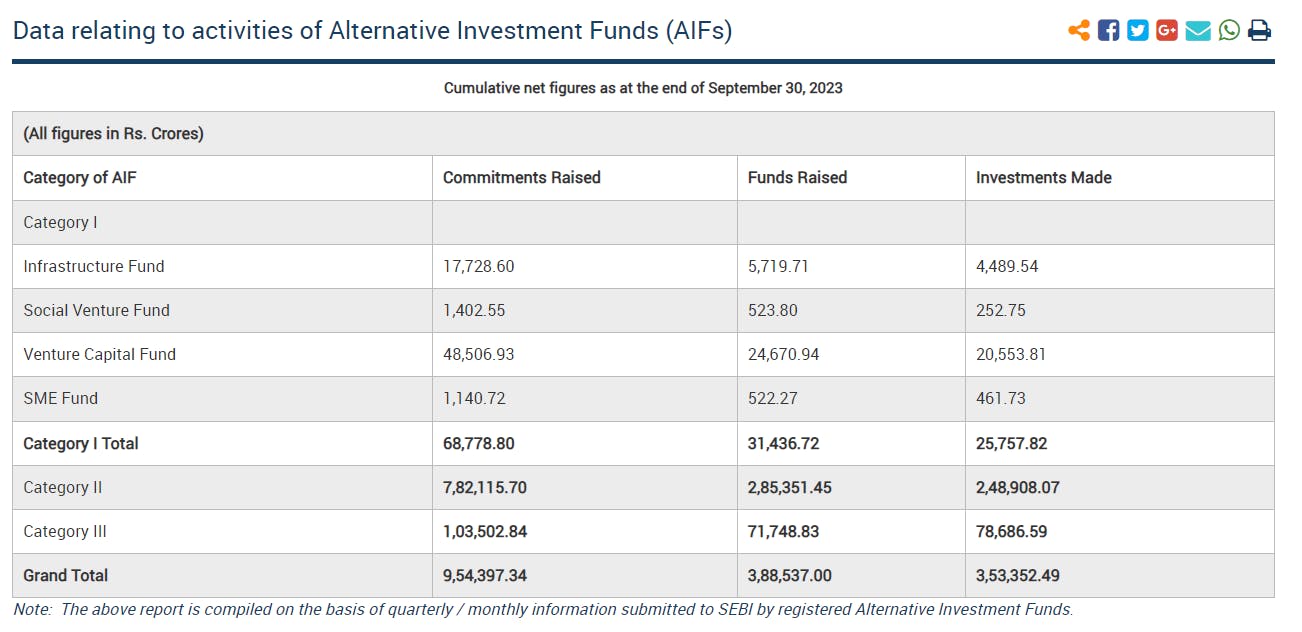

AIFs are fairly nascent in India, and even though the growth numbers are quite impressive there is an obvious catch. To give you guys a picture, in India the current commitments raised by AIFs is roughly ₹10 Lakh Crore, whereas the AUM for mutual funds is ₹51 Lakh Crore. But, the actual money which is invested by AIFs is much lower at around ₹3.6 Lakh Crore.

Source: SEBI

Currently, AIFs in India manage much less as percentage of total Investment asset class, when compared to other developed nations. There are some strong reasons for this -

The minimum investment in AIFs in India is ₹1 Cr. And given that these are long-term risky investment product, this ₹1Cr is most likely your surplus cash lying around the house types and not your core investment corpus.

The AIF industry and the industry where AIFs invest in, both are in growth stages. A major flow from AIFs goes into startups funding and unlisted equities/private equity. And only recently, startup funding and private equity in India is catching pace.

Lets Talk Regulations

Just like any other SEBI regulation, for example - MFs or REITs etc. AIF Regulations also have a lot of nitty-gritties. Every clause is important, and every small number or percentage represents a crucial data, so it's not possible to cover the entire thing here. We will list down few of the important regulations which the general public should be aware about:

Minimum Investment And Corpus

The minimum investment amount is ₹1 Cr and the minimum fund size of AIF has to be ₹20 Cr. For Angel funds, the minimum investment in reduced to ₹25 Lakhs over a period of 3 years, with a corpus of ₹10 Cr. Also, the minimum investment amount for directors, employees and fund managers of AIF is ₹25 lakhs as they understand the risks better.

The maximum number of Investors in a fund is restricted to 1000 people, while the limit is actually reduced for angel funds at 50 people.

Capital Contribution And Continuing Interest

Each scheme should have a certain amount of capital contribution from the sponsors of the fund, this ensures that the people running the fund also have a skin in the game. The continuing interest of sponsors for CAT-1 and 2 AIF should be 2.5% of the fund or ₹5 Cr, whichever is lower. For CAT-3 AIF, sponsors are required to maintain 5% of fund value or ₹10cr whichever is lower.

Audit And Disclosure Norms

The common belief is, AIFs are not required to disclose their portfolio and returns periodically, thus the compliance work is quite less. But this is not exactly true, SEBI mandate certain disclosures that need to be made by the AIF to the investors from time to time. Such disclosure requirements include periodical disclosure of financial, risk management, operational, portfolio and transactional information, and any material liability that arises during the AIF’s tenure.

CAT-1 and CAT-2 AIFs are required to annually provide investors with the financial details of its portfolio companies and information pertaining to any material risks, while in case of CAT-3 AIFs, such reports are to be provided to the investors on a quarterly basis.

Private Placement Memorandum (PPM) and other Norms

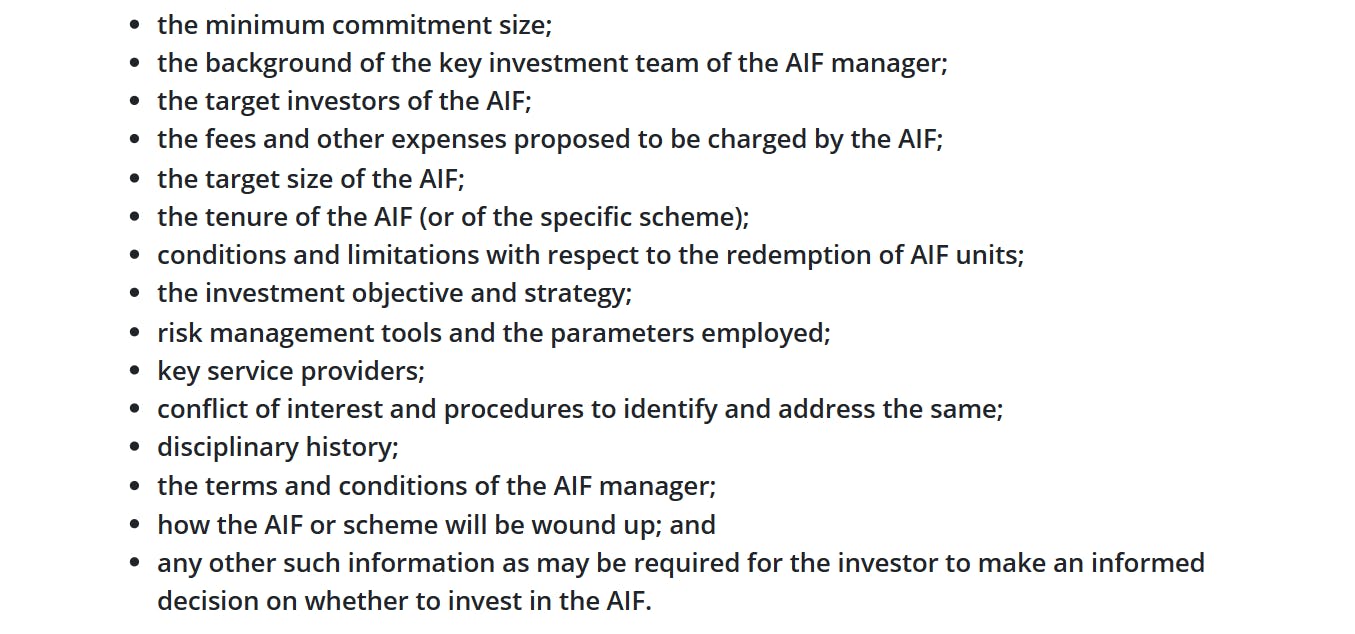

PPM is the document or the marketing material that AIFs prepare for the private placement round. PPM along with all the other marketing materials needs to be registered and approved by SEBI, before displaying it in fundraising. AIFs are not allowed to invite or market schemes to public at large, the fundraising has to done quietly through private placement.

This document is shown to various financial institutions such as pension funds, life insurance companies, endowment funds, banks etc. along with HNIs to raise commitments for the fund. Thus, given this document's importance, SEBI made some PPM norms and other documentation norms to standardize the process of raising funds. These are the details which should be mentioned in a PPM:

Valuation Of Portfolio

According to SEBI, all AIFs have to appoint an independent and IBBI certified valuer to value the portfolio of the AIFs. For funds which are buying and selling debt instruments and listed equity, valuing the portfolio is not a huge problem, as the prices are available in the market. But for schemes which invest in unlisted equity, real-estate or other assets which are not listed and cannot be valued on the buying price or face value, valuing the portfolio become very important. The portfolio value set by the IBBI certified and SEBI approved valuer, will be used to compute the NAV of the unit.

Fund Life And Lock-In Period

Each fund, depending upon the category and whether the fund is close-ended or open-ended, has a different fund-life and lock-in period. Generally, the CAT-1 and 2 will have a lock-in period of 3 years and are compulsorily close-ended funds.

On the other hand, CAT-3 funds can be open or close ended. The minimum duration of close-ended CAT-3 fund is 3 years. Also, the CAT-3 open-ended funds do not have a lock-in period.

There is no maximum duration as such, AIFs may choose to run the fund for 50 years, but they will mention the fund life in the prospectus. SEBI is also planning to put an upper limit on the fund life of such funds.

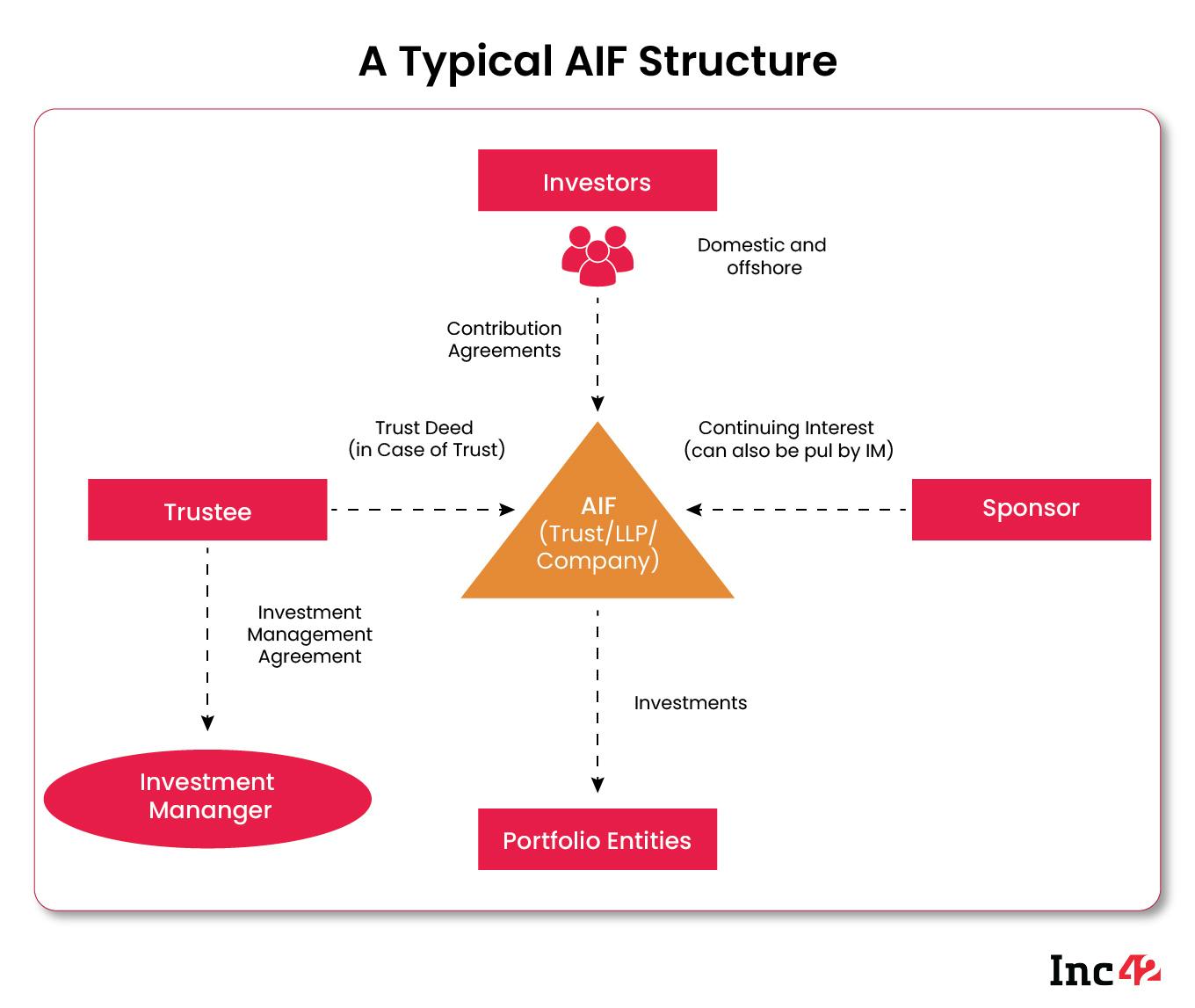

Structure Of AIFs

Structure of AIFs are very similar to MFs in general but AIFs (unlike MFs) can use Trusts, LLPs, Pvt. Ltd Companies to pool funds, but according to SEBI, majority of the AIFs are in the form of a Trust.

The entire story starts with a sponsor, who decides to set up the trust and an AIF to pool money. The sponsor and the asset management company are first vetted by the SEBI and are pronounced eligible and fit to run an AIF, before getting the license. There are several criteria which are considered before granting an AIF license, all of which is explained here.

The sponsor first decides on an AIF scheme, after discussing with fund managers and consultants. The sponsor then files the proposal for AIF scheme with SEBI. Once SEBI gives the go ahead, the sponsor setups up a pooling vehicle, in the form of a Trust, LLP or Pvt. Ltd company (most likely the pooling vehicle will be a trust). The sponsor will also appoint a trustee to manage the operations of the Trust. The trustee will then officially appoint an Investment Manager (IM) under the Investment Management Agreement (IMA) to manage the portfolio allocation of the fund.

Once all of this is done, investors which are gathered through private placements, will invest their money, and the sponsor will contribute its share as a continuing interest in the fund. Both, the investors and sponsors will be given units of the trust in proportion to their investment. According to recent regulations, new investors will receive their units in their demat account.

The Investment Manager (IM) will manage this fund and allocate the portfolio accordingly. The fund will also share portfolio and risk management disclosures with investors and SEBI as per the regulations and Contribution Agreement (CA).

Types Of AIF in India

CAT-1 AIF

CAT-1 AIF Includes funds such as

Angel Funds: Invest in early age/ ideation stage startup. Generally, they do small funding rounds and participate in seed rounds.

Venture Capital: Venture capital are one step above Angel funds, they invest in early age startups, and the fund size is comparatively, quite larger than Angel funds.

SME Funds: As the name suggests invest in small and medium scale enterprise through Fundraising Rounds, IPOs, QIPs and sometimes through debt.

Social Venture Funds: Social Venture Funds are similar to Angel and VC, but are more purpose driven, as they invest in ventures which are solving social problem while also generating financial returns. This includes ventures in solar/ green energy, waste recycling etc.

Infrastructure Funds: Infrastructure Funds invest in companies that are into capex heavy infra business. Companies which are into building highways, dams, bridges, public infrastructure etc, are the main investment for these companies. The instruments are generally QIPs, IPOs, Unlisted and Listed Equities and Debt.

CAT-1 funds are generally categorized as funds which will invest in purpose driven, social and economically viable opportunities.

CAT-2 AIF

CAT-2 fund is essentially residual of CAT-1 and CAT-3. All the funds that did not fit under the other two categories were placed in Cat-2. This Includes:

Private Equity Funds: PE Funds invest in growth/ mature stage companies through fundraising rounds. They are mostly into unlisted equity space.

Structured Credit Funds: They invest in structured debt products such as Interim Financing, Collateralized Debt Obligations (CDOs), Mortgage-Backed securities (MBS) etc. Their aim is to invest in debt products which gives higher yield that plain vanilla bonds, while also gives flexibility and lower risk than equities. They do not invest in debt instruments which are linked to markets.

Debt Funds: CAT-2 Debt funds invest in municipal bonds and corporate bonds.

Real-Estate Funds: As the name suggests, Real-Estate funds invest in high yield investment grade property, such as office complexes, shopping malls, land parcels, etc.

CAT-2 AIFs have always been the largest amongst the AIFs in India, and for past 5 years, it made up on average ~69% of the total AIF AUM.

CAT-2 funds can invest upto 50% in listed securities. These funds have a lower compliance work when compared to CAT-1 a much lower when compared to CAT-3.

CAT-3 AIF

CAT-3 AIF Funds Include:

Long Only Funds: Equity markets fund with long term investment strategy (Buys and hold), usually not participating in trading and F&O.

Long-Short Funds: Equity markets fund with both, long-term investing and short-term trades. They also participate in trading and can buy and short stocks.

Complex Trading And Strategy Funds: Proprietary trading firms with complex strategies.

CAT-3 funds are categorized as funds which invest in equities, with complex investing and trading strategies. CAT-3 AIFs are the only funds which are allowed to take a leverage for investment. They can take leverage up to 2x the fund size.

Fee Structure

At this point, I would have loved to talk about investment returns, but AIFs are not required to disclose their returns publicly, so we will have to directly skip to fee structure. And to be honest, fees structure of AIFs is quite interesting, it's because there is no regulatory limit on the amount of fees charged by AIFs, unlike in mutual fund where there is a limit on total expense ratio. Also, AIF can have multiple share classes of Investors, Class - A unit holders (Generally the sponsor and fund manager), Class - B (General Institutional and HNIs), Class - C...etc. Each of these classes will have their own fee structure, so it's important to check the Contribution Agreement (CA) first.

Talking about the most basic fee structure. If a fund is using the usual 2/20 fee structure with hurdle rate of 12%. It means that every year, the fund will charge 2% as management fees, and if in a year, the fund generates more than 12% return, i.e. the hurdle rate, it will charge success fees of 20% on returns generated above 12%.

Now this is the most basic form, but AIFs like to play with the structure. Some IMs like to charge just charge on the share of entire profits. So, if there is a loss, IMs get nothing, and if the NAV of unit increases by only 2%, they will take their share from the capital appreciation.

Say there in one year, the fund delivered a return of 16%, the other year the return was -16%, and the next year it was 10%. In this case the actual NAV will be much less than the original value, still you would have paid the manager success fees twice. Similarly, in cases where there is Class A, B and C, it is possible that some of these investors are in a profit-sharing model called catch-up. Here, the actual returns could be nil, if the returns are below a set rate. Thus, the contribution agreement becomes essential before investing.Hereis a link for a sample AIF CA.

Taxation

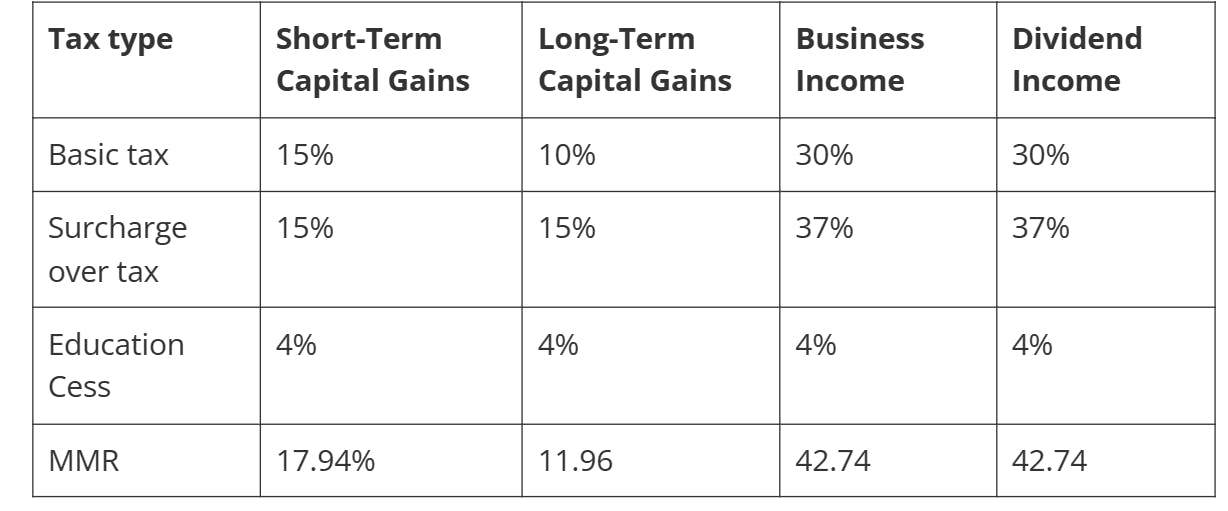

To make things clear, we will go back to 2015 when section 194LBB was inserted in the Income Tax Act. This section gave CAT-1 and 2 AIF, pass-through status, which meant that for any income generate by AIF, other than business income, will be taxed in the hands of investors under section 115UB. And any business income such as capital gains, will be taxed in the on the AIF (fund) level. Such business income will be taxed at the highest marginal slab of the AIF which is 30% + Surcharge + CESS, which comes to around 42.7%.

Now coming to the CAT-3 AIFs, the taxes here are paid on the fund level, thus the returns in the hands of investors is not taxed. the tax is paid depending upon the source of income and the marginal tax bracket the pooling vehicle falls into. CAT-3 AIFs are taxed in the following manner:

Source: Tata Capital

Pros

No Correlation To Markets - One of the key reasons why HNIs want to invest in AIFs is because, the returns are not correlated to market. CAT-1 and CAT-2 do not have any correlation to equity markets, even though interest rate changes may affect the debt funds. Even CAT-3 funds, as they employ complex investment strategies, their returns also do not correlate to larger index.

High Returns - HNIs and institutions flock to AIFs as they promise high returns in a longer timeframe. The returns of AIFs cannot be judged on yearly basis, rather need to be seen in a longer time frame. We cannot really compare the data for returns as AIFs do not publish their returns on public forum.

Diverse Asset Class - This is something you must have guessed by now, AIFs provide access to diverse asset classes such as interim financing, real-estate, trading strategies, startups, structured debt products etc.

Cons

Complicated Products - Even though the investors in AIFs are institutions and sophisticated HNI investors, there is still mis-selling which happens. This is because the products are complicated and have various components to them. Things such as unfair expense ratios, flawed investments, shady underlying assets, needs to be analyzed properly.

No Analyst Coverage - AIFs have no analyst coverage whatsoever, so investors do not know what to expect out of the scheme.

High Investment Amount - Nothing to explain here, we all know the investment amount for AIFs is quite high at minimum ₹1 cr.

Lock-in period and No Liquidity - As we discussed earlier, AIFs have lock-in period of 3 years. And even after lock-in period, in liquidity or the option to liquidate your units is very low.

How to Invest?

If you are an active investor in Mutual fund or invest in IPOs, you would see companies, Investment Banks actively advertising about products, NFOs, IPOs etc. But there are no such ADs for AIFs, why so? Its because AIF schemes are only marketed through private placements or distributed through Banks, life insurance and pension funds. So, if you want to invest in an AIF, either directly connect with the sponsors/IM of the fund or ask your RM from bank or broker.

Conclusion

It is no surprise that most of you reading this article may not even consider AIF due to the minimum ₹1 Cr requirement or ₹25 L for the Angel Fund. These are not small amounts for an average retail investor. But we have seen some platforms launching their own AIFs and marketing to their potential customers that something like AIF exists and we are happy to give you more info if needed.

So we thought it would be fair to just write a detailed piece on AIF which can act as a guide for you if you ever decide to invest and here we are. Like we have discussed above, the AIF market is quite small as compared to it's global peers and we only expect this to grow as investors like you and me chase higher yields with higher risks.

AIFs invest in big ticket sizes and large amount, and if the India growth story holds momentum, it will be a good news for AIFs, as the economy and markets will have a constant vacuum of funds, which can be fulfilled by these AIFs.

Some retail investors have argued by the minimum amount of AIF investment is so high, we think it's a fair number to enter in given the complexity and risks associated with the product where you can lose upto 100% of your capital as well. So the entry barrier stops normal retail investor to enter in.

If you ever have questions on AIF or need help in evaluating an AIF, you can reach out to our team via the community (joining link at start of the article)

We hope you learned something new via this article! We will continue to bring you detailed pieces on various types and platforms of alternatives weekly! Thank you for your support.

Please note that this is an opinion blog and not official research advice. I am not a registered RIA in India. This blog aims to promote informed decision-making and does not discourage you from investing in any deals.

We plan to come up with more blogs discussing different types of instruments available in the world of startup investing, write on due diligence for some platforms, and also existing and upcoming alt investment deals in the Indian market. If you want to stay updated on the latest blogs, please subscribe to our newsletter so you get notified automatically.

Lastly, if you like our work, please feel free to sponsor us via Hashnode Sponsors.